Welcome to THE MAD BRIEF

It only took a few weakening economic data points, a downward revision of US GDP, and a 10% market correction for the big bad 'R' word—recession—to resurface. That reaction seems dramatic, considering the state of economic data over the past two years.

While a recession seems overdue after trillions of dollars in stimulus flooded the system in 2020-2022, I’m not convinced it’s happening for the right reasons just yet.

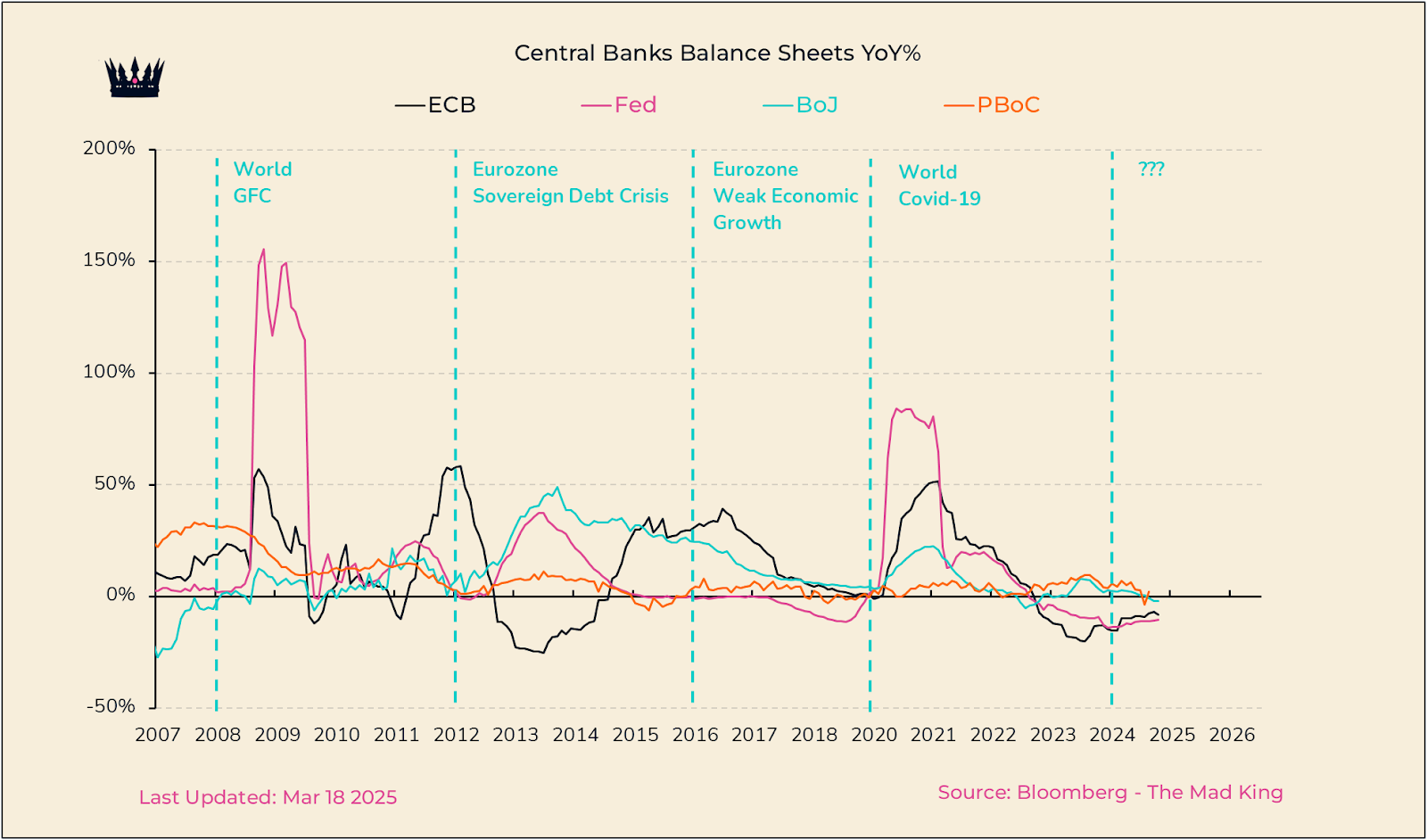

What is clear, however, is that liquidity is lacking, with central banks keeping the money printers off. The harsh reality remains: no money, no rally, and nothing should change until something breaks up.

The liquidity missing in the system is obvious.

Therefore, are we seeing the early signs of a real recession, or is this just the withdrawal effect of markets addicted to liquidity?

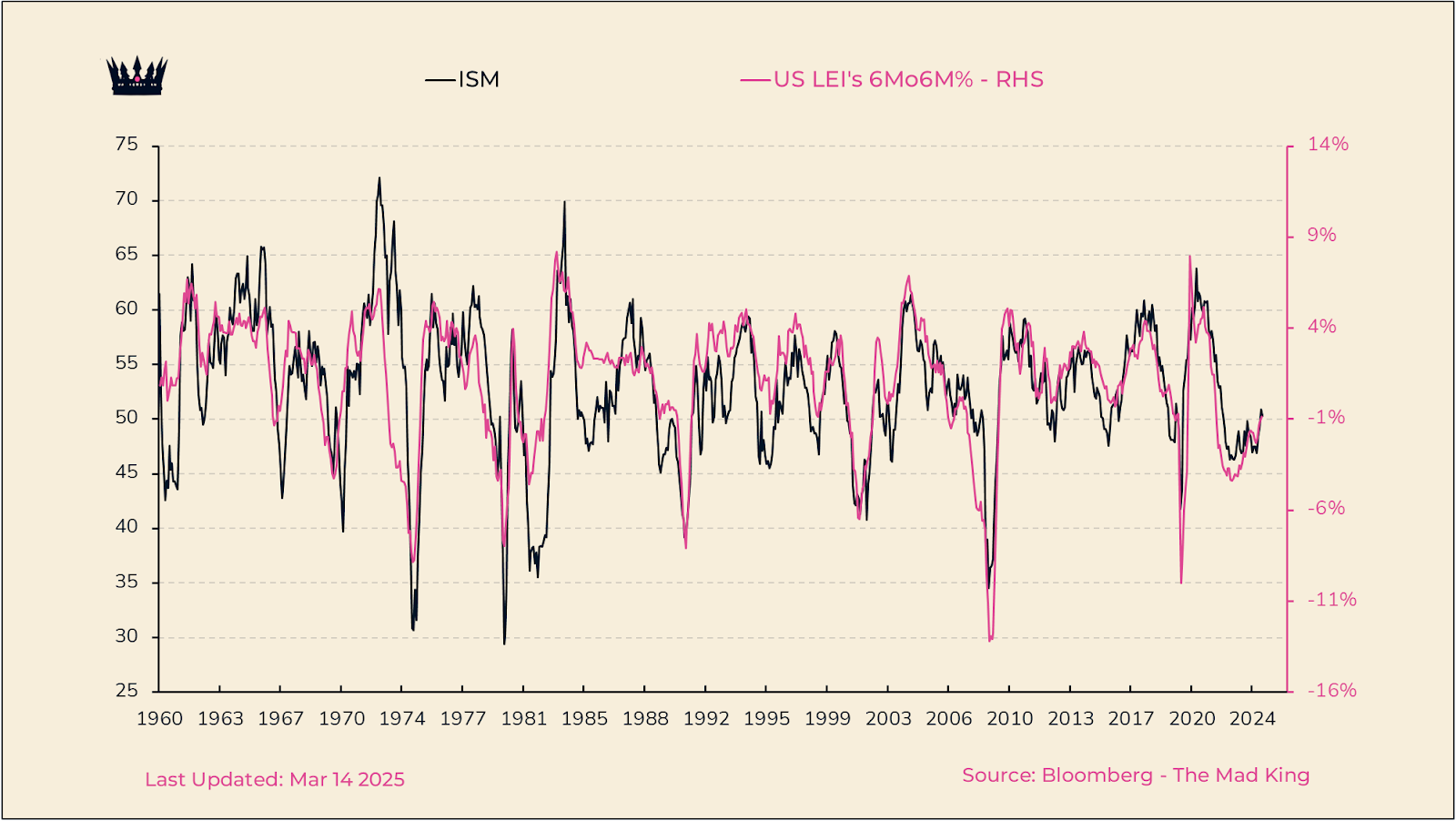

It’s funny how the world works. For two years, the US manufacturing sector and many economic indicators were flashing red, yet many saw the market strength as perfectly normal, even as recession risks were at their peak.

A spate of tariff threats and a little market correction were enough to bring the “R” word back in force, although many economic data, like industrial production, are bouncing.

ISM is expanding for the second consecutive month after two years of contraction…

Leading indicators seem to finally be ready to improve….

I’m not saying a recession isn’t possible; but to be fair, we’ve seen much worse economic data to justify one over the past two years. So far, the economy has managed to handle it—maybe it can hold up for now.

However, it is also easy to find reasons to forecast a recession.

Maybe the yield curve steepening will matter this year…

Maybe contracting consumer credit will impact GDP…

Maybe cutting government spending aggressively will trigger a recession…

Based on their latest forecast revision, the Atlanta Fed clearly sees these factors as significant. We’ll know more soon, but uncertainty is no longer just a market concern—it’s spreading beyond Wall Street.

Which leads us to the natural next question: What is the Fed going to do?

What they usually do and should do if GDP was to contract rapidly is obvious, which leads us to another question: Will they do it fast enough, and be proactive? Personally, I doubt it!

What’s certain is that, driven by expectations, markets will likely react positively to a rate cut—or any news they can spin as bullish—even if they shouldn’t at this stage. However, if the cut comes too late or is too small, the pain could be far from over.

On a short-term horizon, it looks like the US market is approaching a bottom. The current correlation between our REL Index and the S&P 500 suggests year-on-year growth of around 20% for the S&P 500 by April.

Note: Our proprietary REL Index, which blends global demand and financial conditions, is built using gold, oil, shipping stocks, US bonds, and the VIX. It has been highly accurate lately—I’ll present it in the next Mad Brief.

Here’s the thing. Last year, the S&P 500 saw a correction in April, so for annual growth to still land around 20%, it doesn’t actually need a huge rebound.

What’s interesting is that if we do get a bounce now but it falls short of a new all-time high, it could set up a textbook topping pattern. Either way, a technical bounce seems likely.

For now nothing has broken, but the clock is definitely on; and again, this is something I will likely develop further in the next Mad Letter.